.avif)

Editor’s note: This article was written prior to the European Parliament vote on 17 December 2025, which approved a 12-month delay to the implementation of the EU Deforestation Regulation (EUDR). The content is currently under review to reflect this change.

As part of our ongoing EUDR Lunchtime Webinar Series, Anna Roberts, Interu’s Head of Market Development, addressed some of the most common and practical questions we receive from companies navigating the EU Deforestation Regulation (EUDR). One of the key areas of confusion is whether certain products fall in scope of the Regulation. To help clarify, we’ve summarised some of the questions raised on the webinar and the guidance provided during the session.

- Are there any issues if you trade only in the UK?

EUDR obligations apply only when a relevant product is placed on the EU market or exported from the EU. If your goods never enter the EU customs territory (and you don’t export from the EU), EUDR doesn’t apply.

This is because The Regulation only governs placing/making available on the Union market and exporting from the Union (the “Union market” is the EU market).

A number of our customers are UK based and all of their customers are in the UK. However, their customers do trade the products into the EU further downstream. Therefore whilst the UK companies are not directly in scope, if there is a chance that your products will end up in the EU you will need to be prepared to provide supply chain information to the EU companies importing the products.

You might find the scenario diagrams for non-EU companies in this blog useful.

Please also note that under the present Windsor Framework, Northern Ireland is classed as being within the EU for the purposes of EUDR.

- One thing that causes confusion is whether paper mill broke is exempt. Is this classed as a by-product or Post-Industrial Waste (PIW)?

As a general rule of thumb for by-products and waste:

By-products of ongoing production are in scope (no “recycled” exemption); whereas recovered “waste & scrap” products that have completed their lifecycle can be out of scope if the finished product is made entirely from recovered material.

Section 7(b) of the most recent guidance document from the European Commission covers this question:

Operators and traders handle during their economic activities used products that have completed their lifecycle, and which would otherwise be disposed of as waste. Waste means a substance or object which the holder discards or intends or is required to discard (Directive 2008/98/EC, Article 3(1)). Such products are excluded from the scope of the EUDR. This means that such operators and traders are exempted from the obligations of the EUDR in these cases.

This exemption applies to goods that have been produced entirely from a material that has completed its lifecycle and would otherwise have been discarded as waste (e.g. timber retrieved from dismantled buildings, or goods made from coffee chaff).

This exemption does not apply to by-products of a manufacturing process that involves material that is not waste in the sense of being a substance or object which the holder discards or intends or is required to discard.

Therefore, in the case of paper mill broke: if it’s re-pulped internally and not discarded, it behaves like a by-product and is therefore not exempt. If it leaves the mill and is traded as recovered waste & scrap, and a finished paper product is made entirely from that recovered material, that product can be out of scope; any virgin share remains in scope.

This is an example of a question which would be good to raise with your local competent authority (contact details are available here).

- What if I am a EU-based non-SME construction company, constructing apartment buildings that contain various timber products. I am not supplying a relevant product. If all these timber products are bought on the EU market, what obligations are there for me as the construction company?

When you purchase the timber products you are buying in-scope products in the course of a commercial activity. If you are transforming the product, you will be classed as a non-SME operator.

Whilst the apartment buildings themselves, when sold or rented, will not be in scope, you are still obliged to comply with EUDR based on the timber products you buy.

Specifically for a non-SME operator buying only from EU companies, you need to:

- Ascertain that your suppliers have conducted due diligence

- Submit your own DDS to TRACES, referring to the upstream DDS of your suppliers

- Keep records of the due diligence for 5 years

- Share information with your downstream customers

- Report annually on your EUDR due diligence system

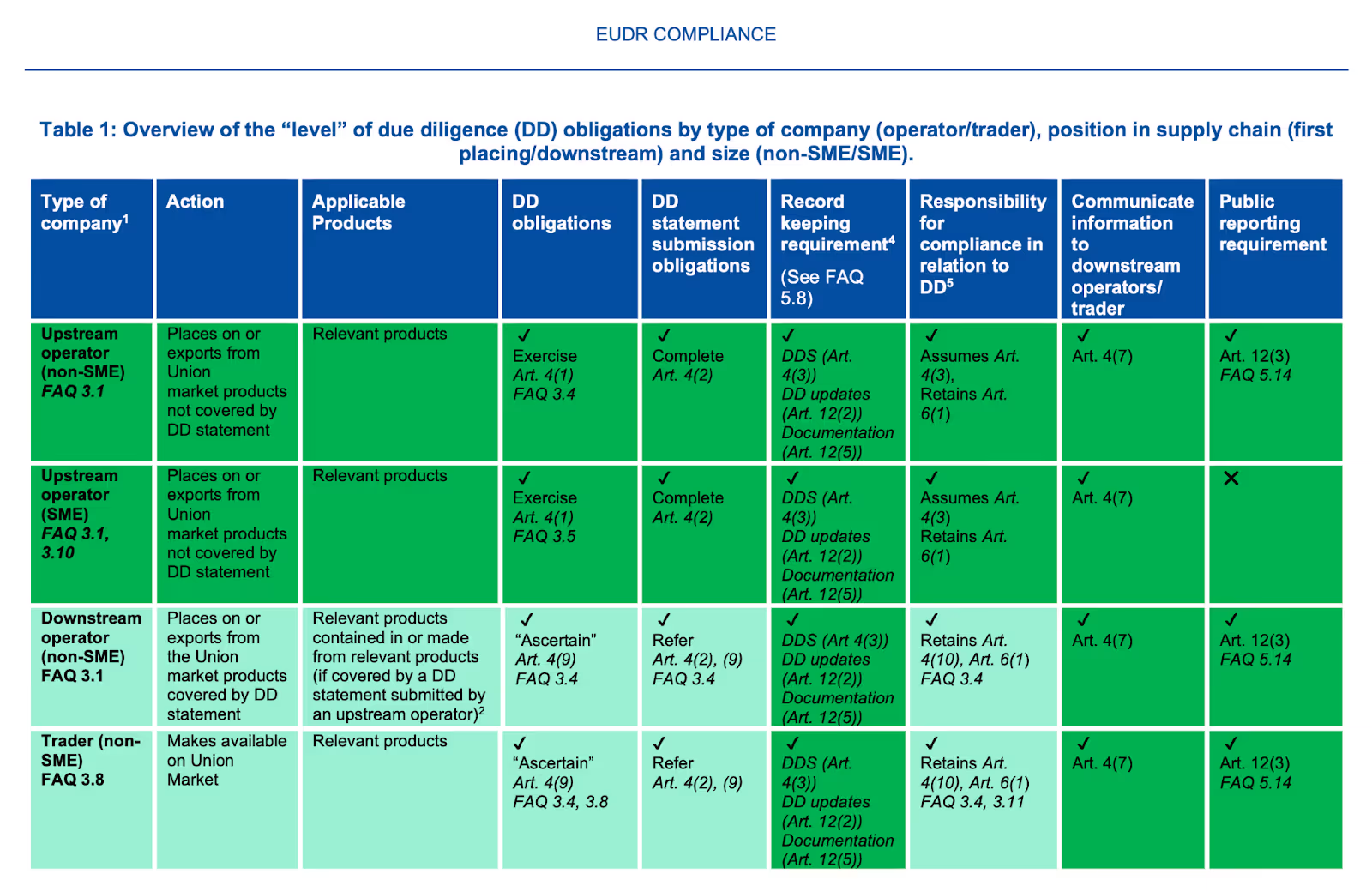

The below table taken directly from an EC published set of scenarios, is very helpful at describing the obligations of different types of companies.

- If the pulp used in manufacturing of paper products was derived from trees felled before Dec 2025 but the paper products were manufactured after 2025, would this be exempt from the scope of EUDR?

This question relates to the transition period. It’s important to determine when the date of production / harvest of the trees was.

If harvested and placed on the market before June 29 2023, the products will be out of scope and can use exemption code Y132.

If harvested between July 2023 and December 2025, and manufactured into paper after 2025, there is also an exemption. This is due to timber, pulp and paper all falling in scope of EUTR. So whilst they do not need to comply with EUDR, they do need to comply with EUTR (up to 31 December 2028).

The most recent official guidance document published by the European Commission in August 2025 covers this exact question in Section 3:

Question: Are paper products which are placed on the market from 30 December 2025 but that are manufactured from timber that was harvested and placed on the market between 29 June 2023 and 30 December 2025 required to have a Due Diligence Statement?

Answer: In such cases the harvested timber and the products manufactured from such timber must comply with EUTR. They do not need a Due Diligence Statement, as this requirement applies to products in scope of EUDR.

Our understanding is that per FAQ 5.4, instead of including DDS numbers, a ‘conventional DDS’ will be issued by the Commission. We have heard that this is likely to be communicated in the next round of clarification, due for publication this month.

- If I understand it correctly, if a material uses goods which if sold individually would be sold using different HS codes (eg a wood product with a palm oil derived coating) only those goods relating to the HS code being used to sell it need to be traced?

Correct. You should always follow the commodity linked to the product’s Annex I entry.

For composite products, operators conduct due diligence on the relevant products listed under the commodity deemed relevant in Annex I for that final CN code.

The Guidance outlines an example using the case of a chocolate bar in Scenario 4d:

A chocolate bar (HS 1806) may contain cocoa and palm oil, but DD is only required for the cocoa products because cocoa is the commodity linked to HS 1806 (summarised)

You must still describe the product per Article 9 and provide geolocation for the relevant commodity included in Annex I.

- Does having certification tracing help, like FSC or PEFC?

Certification can supply complementary evidence for risk assessment, but it doesn’t replace due diligence and doesn’t create a green lane. Operators/traders remain responsible for concluding no/negligible risk and for meeting Article 9 information.

FAQ 5.7 and Section 10 of The Guidance provide more background on the relationship between certification schemes and EUDR. You can also read more in our blog post here.

If you’re unsure whether your products are in scope, or you’d like support in preparing your supply chain for EUDR compliance, get in touch with our team at Interu. We’re here to help you understand your obligations, reduce risk, and ensure your business is ready for what’s ahead.

***

Disclaimer: We provide a portal for the transfer of data from third party sources to individual users. You are responsible for ensuring that your use of the portal, including the data, is sufficient or appropriate for any particular use or circumstances, including taking independent professional advice as necessary. For the avoidance of doubt, you should always seek independent professional advice to confirm your compliance with applicable law.

.jpg)